SCIO briefing on China's financial statistics in H1 2025

Beijing | 3 p.m. July 14, 2025

Speakers

Zou Lan, deputy governor of the People's Bank of China (PBC)

Peng Lifeng, director general of the Credit Policy Department of the PBC

Yan Xiandong, director general of the Statistics and Analysis Department of the PBC

Cao Yuanyuan, deputy director general of the Financial Market Department of the PBC

Chairperson

Speakers:

Mr. Zou Lan, deputy governor of the People's Bank of China (PBC)

Mr. Peng Lifeng, director general of the Credit Policy Department of the PBC

Mr. Yan Xiandong, director general of the Statistics and Analysis Department of the PBC

Ms. Cao Yuanyuan, deputy director general of the Financial Market Department of the PBC

Chairperson:

Ms. Xing Huina, deputy director general of the Press Bureau of the State Council Information Office (SCIO) and spokesperson of the SCIO

Date:

July 14, 2025

Xing Huina:

Ladies and gentlemen, good afternoon. Welcome to this press conference held by the State Council Information Office (SCIO). This is a regular briefing on China's economic data. Today, we have invited Mr. Zou Lan, deputy governor of the People's Bank of China (PBC), who will brief you on the implementation of monetary and credit policies and financial statistics in the first half of the year, and also take your questions. Also joining us today are Mr. Peng Lifeng, director general of the Credit Policy Department of the PBC; Mr. Yan Xiandong, director general of the Statistics and Analysis Department of the PBC; and Ms. Cao Yuanyuan, deputy director general of the Financial Market Department of the PBC.

Now, I'll give the floor to Mr. Zou for his introduction.

Zou Lan:

Good afternoon, friends from the media. Thank you for your continued interest in and support for the work of the PBC. It is my pleasure to have this opportunity to brief you on the implementation of monetary and credit policies as well as financial statistics in the first half of the year. My three colleagues and I will also take your questions.

Since the beginning of this year, the external environment has grown even more complicated and challenging, with weakening global growth momentum and a rise in trade protectionism. In line with the guiding principles of the Central Economic Work Conference and the arrangements set out in the Government Work Report, we need to implement a moderately loose monetary policy. During the press conference held in May, PBC governor Pan Gongsheng elaborated on the concept of a moderately loose monetary policy. In short, this means maintaining sufficient liquidity, ensuring favorable social financing conditions, and keeping overall financing costs relatively low. Policy implementation should adapt to changing circumstances in a timely manner and with the appropriate intensity. From an international perspective, China has been continuously lowering the required reserve ratio (RRR) and interest rates, maintaining a supportive monetary policy stance with cumulative effects. Since 2020, the PBC has cut the RRR 12 times and reduced policy interest rates nine times, driving down the one-year and over-five-year loan prime rates (LPR) by 115 and 130 basis points, respectively.

To implement a moderately loose monetary policy, the PBC further strengthened counter-cyclical adjustments and introduced a package of financial support measures in May. A range of monetary policy tools has been utilized in a comprehensive manner to maintain sufficient liquidity and support reasonable growth in money and credit supply. The market-oriented interest rate regulation framework has been improved to enhance the implementation and oversight of interest rate policies and reduce aggregate financing costs. Greater efforts have been made to leverage both the aggregate and structural functions of monetary policy tools, in a bid to further optimize credit structure, enhance coordination between monetary policy and other macro policies, and create synergy to continuously foster a favorable environment for supporting economic recovery and improvement.

Financial data from the first half of the year shows that the monetary policy has had a clear impact in supporting the real economy. First, overall financial aggregate expanded reasonably. By the end of June, the stock of aggregate financing had increased by 8.9% year on year, the M2 money supply increased by 8.3%, and RMB loans increased by 7.1%. If we remove the impact of replacing local government financing vehicle loans with special-purpose local government bonds, the year-on-year growth of loans would have been ever higher on a comparable basis. Second, aggregate financing costs remained low. From January to June, the weighted average interest rate on newly-issued corporate loans stood at around 3.3%, about 45 basis points lower than the same period last year. The interest rate on newly-issued personal housing loans was approximately 3.1%, down about 60 basis points year on year. Third, the credit structure continued to improve. By the end of May, inclusive loans to micro and small businesses had increased by 11.6% year on year, medium- and long-term lending to the manufacturing sector had grown by 8.8%, and lending to the tech sector had surged by 12%. All of these outpaced the overall loan growth. Fourth, the financial market showed increased resilience. Despite significant changes in the external environment and global financial markets, major financial sectors including equities, bonds and foreign exchange have remained stable.

From both economic theory and practical experience, it is clear that the transmission of monetary policies takes time, and the effects of policies already implemented will continue to unfold. Moving forward, the PBC will continue to implement a moderately loose monetary policy, closely monitoring the transmission and actual impact of policies implemented earlier. Based on the economic and financial situation both at home and abroad, as well as the operation of the financial market, the PBC will properly manage the pace and intensity of policy implementation, in a bid to better expand domestic demand, stabilize social expectations, stimulate market vitality, and support the achievement of this year's socioeconomic development goals and tasks.

That's all from me for now. I will leave more time for questions from the floor.

Xing Huina:

The floor is now open for questions. Please state your news organization before asking your questions.

_ueditor_page_break_tag_CCTV:

The PBC introduced a series of monetary and credit policy measures in the first half of the year. What is the current status of their implementation? Also, what further measures will the PBC take in the second half of the year to promote sustained economic recovery and improvement? Thank you.

Zou Lan:

Thank you for your questions. I think many friends from the media are also closely following these issues. Since the beginning of this year, the PBC has focused on key economic tasks, strengthened the targeting and effectiveness of monetary and credit policies, adopted comprehensive measures, effectively responded to external shocks and promoted economic recovery and improvement.

In terms of monetary policy, we have maintained an appropriately accommodative monetary policy orientation. On May 7, governor Pan Gongsheng announced a package of 10 monetary policy measures. In terms of quantity, we have employed a mix of monetary policy tools, including RRR cuts, to maintain ample liquidity and enhance medium- and long-term liquidity support. In terms of prices, we have emphasized the role of interest rate tools in regulation, lowering policy rates, reducing rates of structural monetary policy tools and individual housing provident fund loans, cracking down on irregular interest rate practices, and strengthening self-discipline in interest rate management. In terms of structure, we have established relending for service consumption and elderly care, increased the relending quota for technological innovation and industrial transformation, created a risk-sharing tool for technological innovation bonds, and intensified support for key areas of domestic demand such as consumption and technological innovation. The package of policies has been fully implemented within one month, playing a positive role in boosting market confidence, stabilizing expectations, and fostering a favorable monetary and financial environment for promoting economic recovery and improvement. Just now, I introduced the financial data for the first half of the year, which also reflects the effectiveness of these policies.

In terms of credit policy, we have strengthened policy guidance and assessment evaluation. We have continued refining the policy framework, promoting the issuance of the Guidance on Advancing the Five Major Tasks, and guiding the financial system to increase credit investment in technology, green, inclusive, elderly care and digital areas. We improved the assessment and evaluation mechanism for the five major tasks, forming a closed-loop process of policy guidance, funding support and performance evaluation. We leveraged finance to help resolve structural imbalances in key industries, promoting quality improvement and upgrading, and reasonably guaranteed the financing needs of foreign trade enterprises in accordance with market-oriented and law-based principles. We also optimized cross-border payment and settlement services to support stable employment and economic stability. By the end of May, green, technology and inclusive loans grew by 27.4%, 12% and 11.2% year on year, respectively, maintaining a relatively rapid growth rate.

In the next stage, the PBC will further implement an appropriately accommodative monetary policy, ensure the implementation of the various monetary policy measures that have been introduced, and improve the quality and efficiency of financial services for the real economy.

In terms of total volume, we will strike a proper balance in the intensity and pace of policy implementation, maintain ample liquidity, ensure that the growth of social financing scale and money supply aligns with the expected targets of economic growth and overall price levels, therefore continuously creating a suitable financial aggregate environment.

In terms of structure, we will highlight the key directions of financial services for the real economy; focus on technological innovation, consumption expansion and private small and micro enterprises; enhance policy coordination; make full use of various structural monetary policy tools; and intensify support for key areas and weak links.

In terms of transmission, we will strengthen the implementation and supervision of interest rate policies, better leverage industry self-discipline, safeguard the competition order in the banking sector, improve the efficiency of fund use, prevent idle fund circulation, and ensure financial support for the real economy while maintaining the soundness of the financial system.

In terms of improving the monetary policy framework, we will further improve the market-oriented interest rate regulation mechanism, optimize the intermediate variables of monetary policy, continuously improve the monetary policy tool system, and establish a credible, normalized and institutionalized policy communication mechanism, so as to better serve high-quality development.

That is all from me. Thank you.

_ueditor_page_break_tag_Elephant News:

How was the total amount and structure of credit in the first half of this year? Thank you.

Zou Lan:

I would like to invite Mr. Yan to answer this question.

Yan Xiandong:

Thank you for your question. Since the beginning of this year, the PBC has earnestly implemented the guiding principles of the Central Economic Work Conference and the deployments of the Government Work Report. We have implemented an appropriately accommodative monetary policy, strengthened counter-cyclical adjustments, comprehensively used various monetary policy tools, and served the high-quality development of the real economy. In terms of effect, credit in the first half of the year was characterized by growth in total volume and structural optimization.

The total amount of credit maintained steady growth. At the end of June, the outstanding balance of yuan-denominated loans held by financial institutions was 268.56 trillion yuan, an increase of 7.1% year on year. In the first half of the year, RMB loans increased by 12.92 trillion yuan, indicating that the financial system maintained a high level of credit support for the real economy. The main characteristics are as follows:

From the perspective of borrowing entities, loans to enterprises and public institutions are the main driver of credit growth. In the first half of the year, loans to enterprises and public institutions increased by 11.57 trillion yuan, accounting for 89.5% of all new loans, up 6.6 percentage points from the same period last year. Of this total, medium- and long-term loans increased by 7.17 trillion yuan, representing the primary component of enterprise and institutional loan growth. This indicates that the financial sector continues to provide stable funding sources for the real economy. Household loans increased by 1.17 trillion yuan, with business loans rising by 923.9 billion yuan, reflecting financial institutions' continued strengthening of support for individual and small business owners' production and business activities.

From the perspective of industry allocation, the sectoral structure of loans continues to improve. New loans are primarily directed toward key areas such as manufacturing and infrastructure. Specifically: At the end of June, the balance of medium- and long-term loans to manufacturing grew 8.7% year on year, increasing by 920.7 billion yuan in the first half of the year. The balance of medium- and long-term loans to infrastructure grew 7.4% year on year, rising by 2.18 trillion yuan in the year's first half.

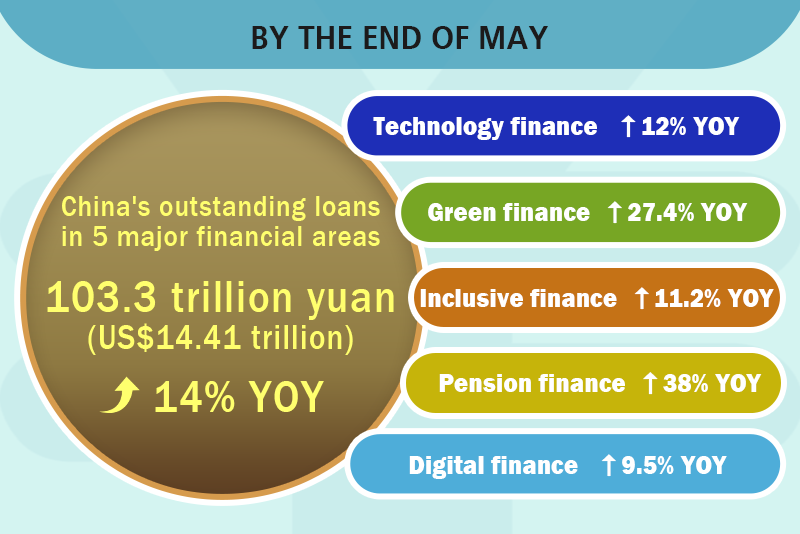

In addition, loans in the five major areas of tech finance, green finance, inclusive finance, pension finance and digital finance have demonstrated both increasing total volume and broader coverage. Strengthening efforts in these five major areas is a key focus for the financial sector to support the high-quality development of the real economy, as well as an important part of deepening supply-side structural reform in the financial sector. In recent years, the PBC has continued to advance the five major areas to better support major strategies, key sectors and weak links. As of the end of May, the balance of loans for the five major areas stood at 103.3 trillion yuan, up 14% year on year. Tech loans, which have drawn significant public attention, had a balance of 43.3 trillion yuan, rising 12% year on year. Among these, the balance of loans to tech-based enterprises reached 22.5 trillion yuan, while those to tech-related industries totaled 32.8 trillion yuan. You may notice that the tech loan balance is lower than the sum of its subcategories because we eliminate overlaps between subcategories when compiling data for the five major financial areas, providing an accurate reflection of our work results. As of the end of May, green, inclusive, pension and digital loans grew 27.4%, 11.2%, 38% and 9.5% year on year, respectively. All of these loan growth rates exceeded the overall loan growth rate for the same period. Financing accessibility has improved significantly. We serve a total of 78.39 million enterprises and individuals, an increase of 5.88 million from the same period last year. Among these, we serve 4.4 million enterprises, an increase of 250,000 from the same period last year.

That's all for my answer. Thank you.

_ueditor_page_break_tag_Bloomberg News:

Many small and medium-sized banks are still investing in bonds aggressively. How does the central bank view their investment risks?

Zou Lan:

I'd like to invite Ms. Cao to answer the question.

Cao Yuanyuan:

First, thank you for your concern about China's bond market. In the first half of this year, China's bond market operated smoothly, with generally stable expectations and steady market growth, effectively supporting financing for the real economy. In the first half of 2025, 44.3 trillion yuan worth of bonds were issued in China's bond market, up 16% year on year. Net bond financing reached 8.8 trillion yuan, accounting for 38.6% of total social financing growth. This provided strong support for the implementation of proactive fiscal policies and financing for brick-and-mortar businesses. In the first half of the year, 13.3 trillion yuan in government bonds, 7.3 trillion yuan in corporate credit bonds and 6 trillion yuan in financial bonds were issued. Bond financing continued flowing toward key areas: more than 350 billion yuan in private enterprise bonds and more than 1 trillion yuan in green and technology-related bonds were issued in the year's first half. In June 2025, the average issuance rate of corporate credit bonds was 2.08%, down 32 basis points from the same period last year, further reducing financing costs for the real economy.

Regarding your concern about small and medium-sized banks' bond investments, bond investment is an essential component of bank assets. In recent years, loans and bonds have accounted for 60% and 25% of total bank assets, respectively, maintaining relative stability. Banks hold 70% of all government bonds and about 20% of all corporate credit bonds, providing strong support for the implementation of fiscal policies and the development of real economy. For small and medium-sized banks, it is reasonable — within regulatory limits — for them to appropriately increase bond holdings and allocate more safe-haven assets based on their own asset allocation strategies, as this helps smooth fluctuations in operating profits. Meanwhile, banks' spontaneous buying and selling of bonds serve as a market stabilizer. When bond rates are relatively high compared to loan rates and bond prices are relatively low, banks will buy bonds, helping to stabilize the market. Conversely, when bond rates are low and bond prices are high, banks selling some bonds can realize profits while maintaining their own sustainability in supporting the real economy.

Of course, we believe that small and medium-sized banks also need to maintain their bond investments at a reasonable level, striking a balance between investment returns and exposure to risk. For financial institutions that take a relatively aggressive approach to individual bond investments, attention should be paid to the interest rate and credit risks faced by the bonds. The PBC will continue to strengthen market monitoring, sharing information on high-risk institutions identified through monitoring with institutional regulatory authorities in a timely manner. We will pay attention to the capital adequacy ratio (CAR) and market risks. At the same time, the PBC will continue to enhance market development by continuously enriching interest rate and credit risk management tools and leveraging market mechanisms to effectively prevent financial market risks.

That is all from me. Thank you for your question.

_ueditor_page_break_tag_Haibao News:

Recently, the PBC and relevant departments introduced guidelines on ramping up financial support to effectively boost consumption. What specifically are the main measures? Thank you.

Zou Lan:

I would like to invite Mr. Peng to answer this question.

Peng Lifeng:

Thank you for your question. Boosting consumption is the top priority for the economic work in 2025. In accordance with the decisions and arrangements of the CPC and the State Council, the PBC, in collaboration with relevant departments, issued guidelines on ramping up financial support to effectively boost consumption. These guidelines aim to direct financial institutions to enhance their services from both supply and demand sides of consumption, so as to fulfill the diverse financing needs of business entities and consumers. It seeks to expand the supply of high-quality consumption and help unleash the potential for consumption growth.

First, supporting the enhancement of consumption capacity and fostering consumption demand. For residents to consume, they need an income, and to have an income, they need jobs. Therefore, stable employment and income growth are fundamental to expanding household consumption. The guidelines focus on supporting employment, increasing residents' income from property, strengthening insurance protection, and other obvious areas of financial support. Specifically, the document proposes thoroughly implementing policies on guaranteed entrepreneurship loans, innovating products for financial wealth management, and optimizing insurance coverage systems for elderly care and health, among other measures.

Second, building a multi-tiered financial service system to support consumption, so as to meet the financing needs of market entities in the consumption sector in all aspects. The guidelines require giving play to the leading role of credit, making good use of refinancing policy tools, and maximizing support for first-time loans, renewal loans, and medium- and long-term loans for eligible business entities. The document also discusses maximizing support for bonds and equities and expanding diversified consumption financing channels.

Third, providing targeted financial support for key areas of consumption to improve the efficiency of financial resource allocation. The guidelines focus on main areas as determined by industry departments, such as commodity consumption, service consumption and new forms of consumption, as well as circulation and other key stages of consumption. It requires financial institutions to innovate financial products in line with consumption contexts and characteristics, and promote the advancement of quality and efficiency of financial services in the consumption sector.

Fourth, strengthening basic financial services to aid the optimization of the consumption environment, and enhancing the willingness and enthusiasm of consumers to consume. The guidelines propose continuous optimization of consumption payment services in food, accommodation, transportation, travel, shopping, entertainment, medical care and other key consumption contexts. They call for improving the establishment of the credit system in the consumption sector and strengthening the protection of financial consumers' rights.

It should be emphasized that service consumption is crucial to boosting overall consumption and expanding domestic demand. It also has an advantage in creating and absorbing employment. Commodity consumption in China is relatively well-developed, as its share of GDP is basically on par with international levels. However, service consumption remains comparatively insufficient and has plenty of room to develop. At present, the service consumption market demand is relatively high, and financial support to meet the demand is generally adequate. The primary obstacle to expanding service consumption, however, lies in supply. Therefore, the PBC has specially established a 500 billion yuan refinancing facility for service consumption and elderly care. The purpose is to guide financial institutions to provide targeted support to accommodation, catering, culture, tourism, sports, entertainment, education, elderly care and other service sectors to increase high-quality supply and make up for the shortcoming. This will give more play to the role of consumption in developing the economy and promote the formation of a positive cycle in which supply creates demand, and demand drives supply.

Going forward, the PBC will work in conjunction with relevant departments to continuously strengthen the coordination of financial, fiscal and industrial policies. We will guide local governments and financial institutions to accelerate the effective implementation of the guidelines, make every effort to enhance financial service for consumption, and provide strong financial support for boosting and expanding consumption. Thank you.

_ueditor_page_break_tag_Market News International:

Recently, the yuan has been appreciating against the U.S. dollar but remains weak against a basket of currencies. How does the PBC view the current performance of the yuan exchange rate? Is there upward pressure on the yuan against the U.S. dollar? And will the central bank take necessary measures to stabilize the exchange rate? Thank you.

Zou Lan:

Thank you for your questions; I will take these. Everyone is closely watching changes in the Federal Reserve's monetary policy. Recently, the growth rate of the U.S. economy has slowed, but the price level remains higher than the Federal Reserve's target. Furthermore, the tariff policy has increased uncertainty in the U.S. inflation trend, affecting the pace and path of the Federal Reserve's interest rate cuts.

The heightened volatility in the U.S. dollar index and U.S. Treasury yields has generated spillover effects across global financial markets. The dollar index has fallen from above 109 at the beginning of the year to around 97, a decline of 11%. The 10-year U.S. Treasury yield briefly rose above 4.8%, marking its highest level since December 2023, but has recently pulled back to around 4.4%. In comparison, China's financial market has shown strong resilience and has been generally stable. The yuan exchange rate against the U.S. dollar experienced some fluctuations in early April but quickly stabilized afterward. Since the release of the joint statement on the China-U.S. Economic and Trade Meeting in Geneva in May, the yuan exchange rate against the U.S. dollar has exhibited two-way fluctuations and remained stable below 7.2.

Multiple factors affect the exchange rate, such as economic growth, monetary policy, financial markets, geopolitics and risk events. Uncertainties persist regarding the future direction of the dollar, but China's domestic fundamentals continue to improve. This provides a solid foundation for the yuan exchange rate to maintain two-way fluctuations and overall stability. First, China's economy has maintained steady growth. GDP in the first quarter increased by 5.4% year on year, which is a good start. On April 25, the meeting of the Political Bureau of the CPC Central Committee made important arrangements concerning economic work, stating that China's economy will sustain the momentum of high-quality development. Second, the market expects the U.S. Federal Reserve to restart interest rate cuts in the year's second half. With major developed economies cutting rates, expectations are mounting for the Federal Reserve to follow suit. This will alleviate the China-U.S. monetary policy misalignment, leading to a narrowing interest rate differential between China and the U.S. Third, a basic equilibrium has been maintained in the balance of payments. In 2024, China's current account surplus represented 2.2% of GDP, within a reasonable and balanced range. China's financial market operates stably while steadily advancing its opening up. Yuan-denominated assets retain their appeal, with cross-border capital flowing in a two-way orderly manner. In the first five months of this year, the net capital inflow from non-bank sectors such as enterprises and individuals was approximately $100 billion. Fourth, significant progress has been made in the development of the foreign exchange market. Market participants have become more sophisticated, trading behaviors have become more rational, and market resilience has significantly increased. In the first half of the year, both the corporate hedging rate and the share of yuan-denominated cross-border trade settlements rose to approximately 30%, indicating a noticeable improvement in enterprises' ability to cope with external shocks.

China will not seek to obtain a global competitive edge through exchange rate depreciation. The PBC's stance on exchange rate policy is clear and consistent. We will continue to uphold the decisive role of the market in exchange rate formation and maintain exchange rate flexibility. At the same time, we will strengthen guidance over expectations, prevent risks of exchange rate overshooting and keep the yuan exchange rate generally stable and at an adaptive and balanced level. Thank you.

_ueditor_page_break_tag_21st Century Business Herald:

This year, the PBC introduced a series of incremental policies to support technology finance and took innovative steps to launch a sci-tech board in the bond market. What is the latest progress and achievements? What are the considerations for the next step? Thank you.

Zou Lan:

We will have Ms. Cao from the Financial Market Department answer this question.

Cao Yuanyuan:

Thank you for your questions. The work on technology finance is crucial for implementing an innovation-driven development strategy and ensuring the financial sector serves the real economy. This year, in accordance with the decisions and plans of the CPC Central Committee and the State Council, the PBC, together with relevant departments, introduced two incremental initiatives. One is the optimization of relending facilities for sci-tech innovation and technical transformation. The other is the launch of a sci-tech board in the bond market. These initiatives have advanced the development of a sci-tech ecosystem through credit, bond and equity channels, achieving good results so far.

First, the relending facility for sci-tech innovation and technical transformation has expanded significantly. The policy has increased in scale, reduced interest rates and broadened coverage. By the end of May 2025, banks have signed agreements for sci-tech innovation and technical upgrading loans totaling 1.7 trillion yuan, 1.9 times that of the end of 2024. Outstanding loans reached 614 billion yuan, supporting 15,000 sci-tech small- and medium-sized enterprises (SMEs) in securing their first-ever bank financing, providing financial support for 3,983 equipment renewal projects in key fields.

Second, the launch of a sci-tech board in the bond market is an innovative measure to support technology finance. It supports the issuance of sci-tech innovation bonds by three types of institutions through differentiated arrangements in the bond issuance and trading systems. That is, financial institutions, sci-tech enterprises and equity investment institutions. As of June 30, since its launch in May, 288 entities in the bond market have issued sci-tech innovation bonds totaling approximately 600 billion yuan, of which over 400 billion yuan were issued in the interbank market. This has not only promoted the cultivation and growth of emerging and future industries but also provided strong support for traditional industries to utilize new technological achievements.

Among the three types of issuers of sci-tech innovation bonds, today I would like to focus on the sci-tech innovation bonds issued by equity investment institutions. As we know, equity investment institutions are a major force for long-term capital investment. They typically invest in early-stage projects, small enterprises and advanced core technologies. However, these institutions are often asset-light entities facing long investment cycles. In the past, such institutions have rarely been financed through bond issuance, and investors were quite cautious about bonds issued by these equity investment institutions. Consequently, their financing costs were relatively high. To facilitate bond issuance by equity investment institutions, we have specifically created a risk-sharing facility for sci-tech innovation bonds. Supported by the PBC's low-cost relending funds, this facility, together with local governments and market-oriented credit enhancement institutions, provides a package of incremental support, including guarantees for bond issuance by equity investment institutions and Credit Risk Mitigation Warrants. In addition, the risk-sharing facility also supports the issuance of sci-tech innovation bonds through direct investment.

As of June 30, a total of 27 equity investment institutions in the interbank market had issued 15.35 billion yuan in sci-tech innovation bonds. Notably, five were privately owned institutions that benefited from credit enhancement through risk-sharing instruments, resulting in three policy effects: First, longer bond terms. Through diversified maturity structures with embedded options, these institutions issued bonds with tenors of five years and even up to 10 years, which better match the characteristics and financing needs of equity investment funds. Second, lower issuance costs. The bond issuance rates for these private institutions were relatively low, ranging from 1.85% to 2.69%, with strong market demand. It should be noted that these bonds were backed by guarantees from risk-sharing tools, so the issuance rates reflect the credit of those tools, significantly reducing financing costs for private equity investment institutions. Third, stronger support for innovation capital formation. The institutions that issued bonds generally have extensive investment experience, strong performance records and excellent management teams. They are key players in early-stage, small-scale, long-term and hard-tech investments. The funds raised through these bonds are used for establishing or expanding private equity investment funds, effectively leveraging the leadership role of fund managers and encouraging greater private capital investment in the technology innovation sector.

Moving forward, the PBC will continue to collaborate with relevant departments to make full use of risk-sharing tools for sci-tech innovation bonds. The central and local governments will coordinate efforts to promote development of the technology innovation bond market. This will help nurture a robust financial ecosystem to support technological innovation and provide stronger financial backing for achieving high-level technological self-reliance. Thank you.

_ueditor_page_break_tag_Red Star News:

What were the key highlights in social financing and money supply growth in the first half of this year? How should we interpret these trends? Thank you.

Zou Lan:

Thank you. Mr. Yan will answer your questions.

Yan Xiandong:

Since the beginning of the year, the PBC has thoroughly implemented the decisions and arrangements of the CPC Central Committee and the State Council, adopting a moderately accommodative monetary policy while maintaining ample liquidity.

Financial aggregate data for the year's first half showed that social financing scale and money supply grew steadily, matching expectations for economic growth and overall price levels. By the end of June, China's social financing scale and broad money supply (M2) both posted year-on-year growth of 8.9% and 8.3% respectively, up 0.8 and 2.1 percentage points from the same period last year.

Aggregate social financing grew at a reasonable pace, with the financial system effectively meeting the funding needs of the real economy. In the first half, the increment in aggregate social financing totaled 22.83 trillion yuan, up 4.74 trillion yuan year on year. On the one hand, proactive fiscal policy took effect early, with the financial system strengthening coordination, leading to substantial year-on-year growth in government bond financing. In the first half, net government bond financing reached 7.66 trillion yuan, up 4.32 trillion yuan year on year. Of this, net treasury bond financing totaled 3.37 trillion yuan, up 1.8 trillion yuan year on year, while net local government bond financing reached 4.29 trillion yuan, up 2.52 trillion yuan year on year. On the other hand, financial institutions maintained solid credit support for the real economy. In the first half, financial institutions extended 12.74 trillion yuan in new yuan-denominated loans to the real economy, up 279.6 billion yuan year on year.

M2 rebounded from the same period last year, maintaining ample liquidity. First, government bonds were issued earlier, leading to increased bond investments by financial institutions and corresponding increases in money creation. In the first half, with heavy government bond issuance, financial institutions' bond investments increased 6.01 trillion yuan, up 3.19 trillion yuan year on year. Second, steady credit growth also supported money creation. Additionally, measures to address capital circulation last year resulted in a lower monetary base in the same period last year. This year, corporate deposit growth recovered, driving up money supply growth. In the first half, corporate deposits increased 1.77 trillion yuan, up 3.22 trillion yuan year on year.

Overall, financial aggregates grew at a reasonable pace in the first half, providing strong support for the real economy's recovery and improvement. Thank you.

_ueditor_page_break_tag_Economic Daily:

What was the financing situation for small- and medium-sized enterprises (SMEs) and private companies in the first half of this year? Looking ahead, what steps will the PBC take to strengthen financial support for these businesses? Thank you.

Zou Lan:

Thank you. Mr. Peng will answer your questions.

Peng Lifeng:

Thank you for your questions. Financing support for SMEs and private companies is a crucial part of promoting inclusive finance and achieving common prosperity. In recent years, the PBC, following decisions and arrangements made by the CPC Central Committee and the State Council, has focused on inclusive finance, especially for SMEs and private companies. Starting from policy guidance, funding support and capacity building, we have continuously improved the institutional mechanisms that enhance access to affordable and convenient financing.

First, we have intensified financial support for SMEs and private companies. One major step has been implementing the 25-point plan to strengthen financial support for the private economy. We've also strengthened financial service capacity, conducted regular assessments of policy outcomes and guided financial institutions to uphold the principle of treating all enterprises equally. As of the end of May, the balance of inclusive loans to micro and small enterprises stood at 34.42 trillion yuan, up 11.6% year on year, with an average annual growth rate of more than 20% over the past five years. Meanwhile, loans to privately controlled enterprises totaled 44.95 trillion yuan.

Second, we have worked to steadily reduce financing costs for SMEs and private companies. We have deployed various monetary policy tools to maintain ample liquidity and continued leveraging the effectiveness of Loan Prime Rate (LPR) reform and the market-based deposit rate adjustment mechanism. We have launched pilot programs to improve transparency around overall corporate loan financing costs, aiming to steadily lower comprehensive financing costs for privately held enterprises and micro and small businesses. In May, the weighted average interest rates for newly issued inclusive loans to micro and small enterprises and loans to private enterprises stood at 3.69% and 3.45%, respectively — down 0.66 and 0.6 percentage points year on year.

Third, we have supported more diversified financing channels for SMEs and private companies. We have leveraged the amplifying and guiding role of the bond financing support instruments for private enterprises, providing credit enhancement for their bond issuance. Financial institutions have been encouraged to issue financial bonds dedicated to supporting micro and small enterprises, with the funds raised earmarked specifically for that purpose. We have also established, improved and actively promoted a unified registration and publicity system for movable assets and rights-based collateral to facilitate financing for SMEs.

Looking ahead, the PBC will focus on the following areas to further enhance financial services for SMEs and private companies.

First, we will further improve the policy framework for financial support to private enterprises and micro and small businesses. We will launch financial service capacity enhancement programs and guide reasonable growth in inclusive micro and small business loans and private economy loans. We will strengthen the credit enhancement system for private SMEs, fully leveraging the positive role of government-backed financing guarantees, information sharing and financial derivatives to improve corporate financing accessibility.

Second, we will continue to increase financial resource allocation. We will implement a moderately accommodative monetary policy and make good use of structural monetary policy tools such as relending for agriculture and small businesses, as well as relending for technological innovation and technical transformation. We will promote well-regulated development of supply chain finance and strengthen financial support for private micro, small and medium enterprises (MSMEs).

Third, we will help enterprises achieve efficient financing connections. We will strengthen communication and cooperation with industry competent authorities to help financial institutions improve the efficiency of financing matchmaking. We will comprehensively promote the national credit information sharing platform for MSMEs' cash flows, supporting precise delivery of credit funds to underserved areas, such as first-time borrowers, start-ups and small businesses. Thank you.

Xing Huina:

We have time for one final question. Please raise your hand if you'd like to ask it.

_ueditor_page_break_tag_Financial Times:

How have structural monetary policy tools been rolled out so far? Are there plans to introduce new ones or raise existing quotas this year? Thank you.

Zou Lan:

I'll answer this question. Based on the goals and requirements for high-quality economic development, the PBC has drawn on international experience in recent years and combined it with domestic realities. While implementing macroeconomic policy, we have extensively created and implemented structural monetary policy tools around supporting major national strategies, key sectors and weak links to further enhance the adaptability and precision of financial services for economic structural adjustment and high-quality economic development. Structural policy tools have achieved full coverage of all five major areas in the financial sector while also providing strong support for the steady and healthy development of the real estate market, capital market and other sectors.

In May, the PBC introduced another package of financial policy measures, many of which were structural policy tools aimed at further supporting economic structural transformation and upgrading.

First, we introduced the service consumption and elderly care relending facility and the sci-tech innovation bond risk-sharing instrument. The service consumption and elderly care relending facility has a quota of 500 billion yuan, specifically designed to incentivize and guide financial institutions to increase financial support for key areas of service consumption and the elderly care industry, which Mr. Peng just introduced. Meanwhile, the sci-tech innovation bond risk-sharing instrument supports equity investment institutions in issuing sci-tech innovation bonds for financing, while also supporting the construction of the bond market's "sci-tech board."

Second, in terms of scale, quotas for certain tools were increased and optimized. An additional 300 billion yuan each was allocated to the relending facility for technological innovation and upgrading and the relending facility for agriculture and small businesses. Meanwhile, the 500 billion yuan quota for the securities, funds and insurance companies swap facility and the 300 billion yuan quota for relending to support stock repurchases and shareholding increases have been merged for more flexible use.

Third, in terms of pricing, relending interest rates were lowered. The interest rates for relending facilities supporting agriculture and small businesses, pledged supplementary lending and various targeted structural monetary policy tools were all reduced by 25 basis points.

All of these structural policy measures were fully launched by the end of May and have continued to deliver positive effects. For example, by the end of May, the total contracted amount of loans for technological innovation and upgrading had reached 1.74 trillion yuan, with enterprises able to draw down funds as needed. The sci-tech innovation bond risk-sharing instrument has provided effective credit enhancement support for equity investment institutions to issue bonds for financing. By the end of June, 27 equity investment institutions had issued sci-tech innovation bonds in the interbank market, totaling over 15 billion yuan.

Moving forward, we will continue to leverage both the aggregate and structural functions of monetary policy tools. Structural monetary policy instruments will continue to focus on key sectors, adopt reasonable and moderate approaches, and build up ample room for maneuver. Building on the support for the five major areas in the financial sector, these tools will place greater emphasis on supporting core priorities such as technological innovation and boosting consumption. This will further enhance their effectiveness in promoting economic restructuring, transformation and upgrading, and the shift from old to new growth drivers. Thank you.

Xing Huina:

That concludes today's press conference. Thank you to Mr. Zou and our speakers, as well as our media colleagues. Goodbye!

Translated and edited by Zhu Bochen, Zhang Junmian, You Jiaxin, Li Congrong, Mi Xingang, Yang Chuanli, Huang Shan, Wang Mianyi, Li Huiru, Xu Kailin, Wang Qian, Cui Can, Li Xiao, Wang Xingguang, Zhang Rui, David Ball, and Jay Birbeck. In case of any discrepancy between the English and Chinese texts, the Chinese version is deemed to prevail.

/6 Xing Huina

/6 Zou Lan

/6 Peng Lifeng

/6 Yan Xiandong

/6 Cao Yuanyuan

/6 Group photo

SCIO briefing on China's import and export in H1 2025

July 14, 2025SCIO briefing on China's economic and social achievements during the 14th Five-Year Plan period

July 9, 2025SCIO briefing on promoting comprehensive river protection and management

July 4, 2025