.

Read in Chinese

Speaker:

Liu Aihua, spokesperson of the National Bureau of Statistics (NBS), director general of the Department of Comprehensive Statistics of the NBS

Chairperson:

Xing Huina, deputy head of the Press Bureau of the State Council Information Office (SCIO) and spokesperson for the SCIO

Date:

July 15, 2021

Xing Huina:

Friends from the media, good morning. Welcome to this press conference held by the State Council Information Office (SCIO). We are joined by Ms. Liu Aihua, spokesperson of the National Bureau of Statistics (NBS) and director general of the Department of Comprehensive Statistics of the NBS. Ms. Liu will first introduce the details concerning China's economic performance in the first half of 2021 and then answer your questions.

Now, let's give the floor to Ms. Liu.

Liu Aihua:

Good morning, I'll start by briefing you all on China's economic performance in the first half of this year and then take your questions.

In the first half of the year, the steady and sound growth momentum of the national economy was further consolidated. In the first half of this year, faced with a complicated and changing environment both at home and abroad, under the strong leadership of the CPC Central Committee with Comrade Xi Jinping at its core, all regions and departments strictly implemented the decisions and arrangements made by the CPC Central Committee and the State Council, continued to consolidate the achievements made in the epidemic prevention and control and the economic and social development, and implemented accurate macro policies. China's economy sustained a steady recovery with both production and demand picking up, employment and prices remaining stable, new driving forces beginning to quickly thrive, quality and efficiency enhancing, market expectations improving and major macro indicators staying within a reasonable range. The steady and sound growth momentum of the national economy was further consolidated.

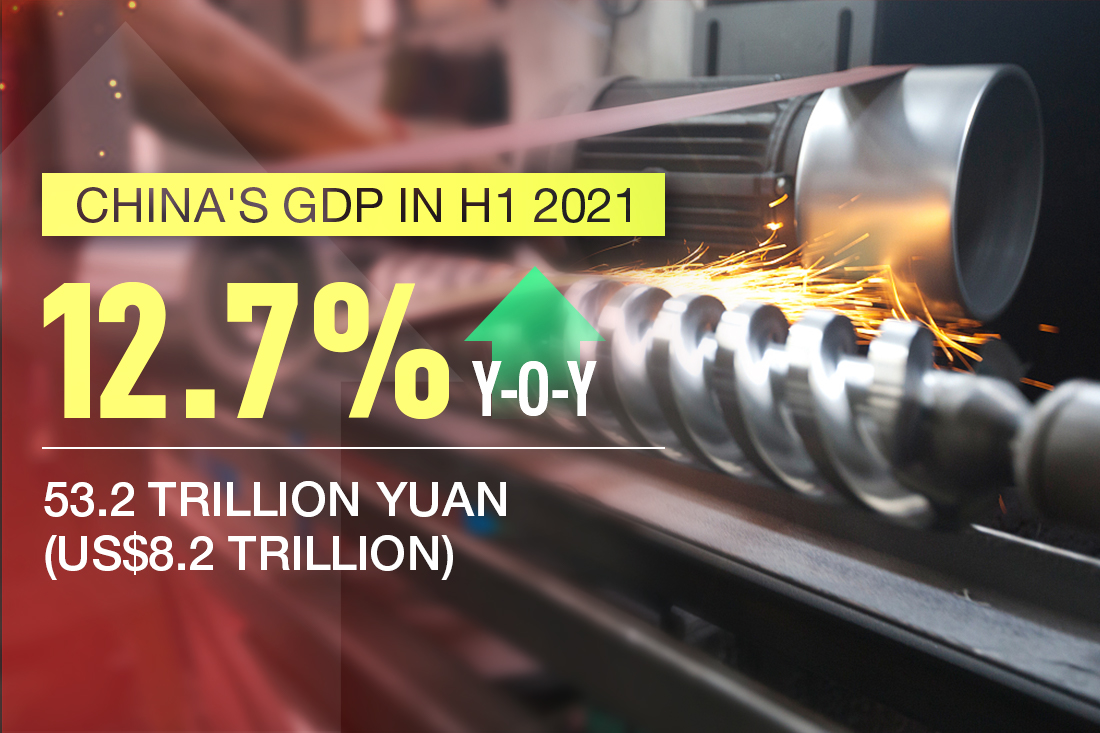

According to the preliminary estimates, the gross domestic product (GDP) of China in the first half of the year was 53.22 trillion yuan, a year-on-year increase of 12.7% at comparable prices, 5.6 percentage points lower than that of the first quarter. Meanwhile, the average two-year growth was 5.3%, a 0.3 percentage points faster than that of the first quarter. By quarter, the year-on-year GDP growth for the first quarter was 18.3%, with an average two-year growth of 5%; and it was 7.9% for the second quarter, with an average two-year growth of 5.5%. By industry, in the first half of the year, the value added of primary industry was 2.84 trillion yuan, a year-on-year growth of 7.8%, with an average two-year growth of 4.3%; secondary industry was 20.72 trillion yuan, a year-on-year growth of 14.8%, with an average two-year growth of 6.1%; and the tertiary industry was 29.66 trillion yuan, a year-on-year growth of 11.8%, with an average two-year growth of 4.9%. The quarter-on-quarter GDP growth of the second quarter was 1.3%.

First, summer grain witnessed another bumper harvest, while production of animal husbandry grew steadily.

In the first half of the year, the value added of agriculture (crop farming) went up by 3.6% year-on-year, a 0.3 percentage points faster than that of the first quarter, with an average two-year growth of 3.7%. Specifically, in the second quarter it grew by 3.7%, a 0.4 percentage points faster than that of the first quarter. The overall output of summer grain was 145.82 million tons (291.6 billion jin), 2.97 million tons (5.93 billion jin) higher than that of last year, an increase of 2.1%. The structure of crop farming continued to be optimized, as sown areas for cash crops like rapeseeds increased. In the first half of the year, the output of pork, beef, mutton, and poultry was 42.91 million tons, up by 23% over the same period last year. Specifically, the output of pork increased by 35.9%; milk rose up by 7.6%; and eggs were down by 4.1%. By the end of the second quarter, 439.11 million pigs were registered in stock, a year-on-year growth of 29.2%. Specifically, 45.64 million were breeding sows, up by 25.7%.

Second, industrial production grew steadily and high-tech manufacturing grew fast.

In the first half of the year, the total value added of industrial enterprises above the designated size grew by 15.9% year-on-year, with an average two-year growth of 7%, a 0.2 percentage points faster than that of the first quarter. Specifically, that of the second quarter went up by 8.9% year-on-year. In June, the total value added of industrial enterprises above the designated size grew by 8.3% year-on-year, with an average two-year growth of 6.5%; and a month-on-month growth of 0.56%. In terms of sectors, in the first half of the year, the value added of mining went up by 6.2% year-on-year, with an average two-year growth of 2.5%; manufacturing was up by 17.1%, with an average two-year growth of 7.5%; and production and supply of electricity, thermal power, gas and water went up by 13.4%, with an average two-year growth of 6%. The value added of high-tech manufacturing went up by 22.6% year-on-year, with an average two-year growth of 13.2%. In terms of products, the production of new-energy automobiles, industrial robots and integrated circuits increased by 205%, 69.8%, and 48.1% year-on-year respectively, with average two-year growth all exceeding 30%. An analysis by types of ownership showed that the value added of the state holding enterprises went up by 11.9% year-on-year; share-holding enterprises went up by 15.8% year-on-year; enterprises funded by foreign investors and investors from Hong Kong Special Administrative Region (SAR), Macao SAR, and Taiwan were up by 17% year-on-year; and private enterprises were up by 18.3% year-on-year. In June, the Manufacturing Purchasing Managers' Index of China was 50.9%, staying above the threshold for 16 months in a row. The Production and Operation Expectation Index was 57.9%.

In the first five months, the total profits made by industrial enterprises above the designated size were 3.42 trillion yuan, up by 83.4% year-on-year, with an average two-year growth of 21.7%. The profit rate of the business revenue of industrial enterprises above the designated size was 7.11%, 2.05 percentage points higher than that of the first five months of 2020.

The service sector recovered steadily with market expectation picking up.

The first half of the year witnessed a steady recovery of the tertiary industry. Specifically, the value added of the tertiary industry for the second quarter increased by 8.3% year-on-year, with an average two-year growth of 5.1%; that for the first quarter increased by 15.6% year-on-year, with an average two-year growth of 4.7%. Specifically, in the first half of the year, the value added of transportation, storage and postal services and information transmission, software and information technology services increased by 21% and 20.3% year-on-year respectively, with average two-year growth increasing by 6.9% and 17.3% respectively. In June, the Index of Services Production increased by 10.9% year-on-year, with an average two-year growth rate of 6.5%. In the first five months, the business revenue of service enterprises above the designated size went up by 31.9% year-on-year, with an average two-year growth of 11.1%, a 0.2 percentage points higher than that of the first four months.

In June, the Business Activity Index for services was 52.3%, staying above the threshold for 16 months in a row. Specifically, the Business Activity Index for sectors closely related with online consumption such as express mail services, telecommunication, broadcast, television and satellite transmission services, internet, software and information services stayed within the expansion range of 57% and above. Monetary and financial services and insurance stood within the expansion range of 60% and above. In terms of market expectation, the Business Activities Expectation Index was 60.4%, continuing to stay within the expansion range.

Fourth, market sales improved gradually and sales of upgraded consumer goods witnessed accelerated growth.

In the first half of this year, the total retail sales of consumer goods reached 21.19 trillion yuan, up by 23% compared with the previous year, registering a two-year average growth of 4.4%, 0.2 percentage point faster than that of the first quarter; and the total retail sales of the second quarter went up by 13.9% year-on-year, with a two-year average growth of 4.6%. In June, the total retail sales of consumer goods reached 3.76 trillion yuan, up by 12.1% year-on-year, with a two-year average growth of 4.9%, and up by 0.70% month-on-month. In the first half of this year, in terms of regions, the retail sales of consumer goods in urban areas reached 18.41 trillion yuan, up by 23.3% year-on-year, with a two-year average growth of 4.4%, and the retail sales of consumer goods in rural areas stood at 2.78 trillion yuan, up by 21.4%, with a two-year average growth of 4%. Grouped by consumption patterns, the retail sales of goods reached 19.02 trillion yuan, up by 20.6% year-on-year, with a two-year average growth of 4.9%; catering revenue was 2.17 trillion yuan, up by 48.6% year-on-year and basically the same as that of the first half of 2019. Grouped by categories, the year-on-year growth rates for 18 categories of goods by enterprises above the designated size all exceeded 10%, among which, over 70% of categories of goods witnessed year-on-year growth rates exceeding 20%. In terms of the two-year average growth, excluding petroleum products, retail sales of other categories of goods all witnessed positive growth, among which, the two-year average growth rates of nine categories, including sports and recreational articles, communication equipment, cosmetics, and cultural and office supplies, exceeded 10%. Online retail sales reached 6.11 trillion yuan, with a year-on-year growth of 23.2% and a two-year average growth of 15%, 1.5 percentage points faster than that of the first quarter. Specifically, the online retail sales of physical goods reached 5.03 trillion yuan, up by 18.7%, with a two-year average growth of 16.5%, 1.1 percentage points faster than that of the first quarter. This accounted for 23.7% of the total retail sales of consumer goods, 1.8 percentage points higher than that of the first quarter.

Liu Aihua:

Fifth, investment in fixed assets continued to recover and the two-year average growth of investment in manufacturing sector accelerated.

In the first half of this year, the investment in fixed assets (excluding rural households) reached 25.59 trillion yuan, up by 12.6% year-on-year, and it grew by 0.35% month-on-month in June. The two-year average growth rate reached 4.4%, 1.5 percentage points faster than that of the first quarter. In terms of sectors, in the first half of this year, investment in infrastructure was up by 7.8% year-on-year, with a two-year average growth of 2.4%, a slight decrease compared with the first five months. Investment in manufacturing was up by 19.2% year-on-year, with a two-year average growth of 2.0%, 1.4 percentage points faster than that of the first five months. Real estate development was up by 15% year-on-year, with a two-year average growth of 8.2%, a slight decrease compared with the first five months. The floor space of commercial buildings sold reached 886.35 million square meters, up by 27.7% year-on-year, with a two-year average growth of 8.1%. The total sales of commercial buildings reached 9.29 trillion yuan, up by 38.9% year-on-year, with a two-year average growth of 14.7%. In terms of industries, investment in the primary industry went up by 21.3% year-on-year, with a two-year average growth of 13.2%. Investment in the secondary industry was up by 16.3% year-on-year, with a two-year average growth of 2.9%. Investment in the tertiary industry was up by 10.7% year-on-year, with a two-year average growth rate of 4.8%. Private investment was up by 15.4% year-on-year, with a two-year average growth rate of 3.8%. Investment in high-tech industries grew by 23.5% year-on-year, with a two-year average growth of 14.6%, of which the investment in high-tech manufacturing and high-tech services increased by 29.7% and 12% year-on-year respectively and their average two-year growth rates reached 17.1% and 9.5% respectively. In terms of high-tech manufacturing, investment in the manufacturing of computers and office equipment and in the manufacturing of medical equipment, measuring instruments and meters grew by 47.5% and 34.2% year-on-year respectively and their two-year average growth rates reached 26.3% and 18.7% respectively. In terms of high-tech services, the investment in e-commerce services and in research, development and design services went up by 32.9% and 28.4% year-on-year and their two-year average growth rates reached 32.5% and 15.9%. The investment in social sectors went up by 16.4% year-on-year, with a two-year average growth rate of 10.7%, among which the investment in health and education went up by 35.5% and 14.2% year-on-year, with a two-year average growth of 24.9% and 12.5% respectively.

Sixth, imports and exports of goods grew fast and the trade structure continued to optimize.

In the first half of this year, the total imports and exports of goods expanded by 27.1% year-on-year to reach 18.07 trillion yuan. The total value of exports was 9.85 trillion yuan, up by 28.1% year-on-year. The total value of imports was 8.22 trillion yuan, up by 25.9% year-on-year. The trade balance was 1.63 trillion yuan in surplus. The trade structure continued to improve. In the first half of this year, the exports of mechanical and electrical products accounted for 59.2% of the total value of exports, up by 0.6 percentage point over the same period last year. The imports and exports of general trade accounted for 61.9% of the total value of imports and exports, up by 1.7 percentage points over the same period last year. The imports and exports by private enterprises accounted for 47.8% of the total value of imports and exports, up by 2.8 percentage points over the same period last year. In June, the total value of imports and exports was 3.29 trillion yuan, an increase of 22% year-on-year. The total value of exports was 1.81 trillion yuan, up by 20.2% year-on-year. The total value of imports was 1.48 trillion yuan, up by 24.2% year-on-year.

_ueditor_page_break_tag_

Liu Aihua:

Seventh, consumer prices rose mildly and producer prices for industrial products remained at a high level.

The consumer price index (CPI) went up by 0.5% year-on-year in the first half of this year, while remaining flat year-on-year in the first quarter. In June, consumer prices went up by 1.1% year-on-year, 0.2 percentage point slower than May, and down by 0.4% month-on-month. In the first half of this year, consumer prices went up by 0.6% in urban areas and 0.4% in rural areas. Grouped by commodity categories, prices for food, tobacco and alcohol were up by 0.4% year-on-year; clothing remained the same year-on-year; housing was up by 0.2%; articles and services for daily use were up by 0.1%; transportation and communication were up by 1.9%; education, culture and recreation were up by 0.9%; medical services and health care were up by 0.3%; and other articles and services went down by 1.1%. In terms of food, tobacco and alcohol prices, prices for pork went down by 19.3%, grain was up by 1.2%, fresh fruits were up by 2.6% and fresh vegetables were up by 3.2%. Core CPI, excluding the prices of food and energy, went up by 0.4%, after remaining the same year-on-year in the first quarter.

In the first half of this year, producer prices for industrial products went up by 5.1% year-on-year, 3 percentage points faster than the first quarter. In June, it grew by 8.8% year-on-year, 0.2 percentage point slower than in May. In the first half of this year, the purchasing prices for industrial producers went up by 7.1% year-on-year, 4.3 percentage points faster than the first quarter. It went up by 13.1% year-on-year and 0.8% month-on-month in June.

Eighth, the surveyed unemployment rate in urban areas was the same as last month and employment was generally stable.

In the first half of this year, 6.98 million new jobs were created in urban areas, which meant that 63.5% of the whole year target was achieved. In June, the surveyed unemployment rate in urban areas was 5%, the same as in May and 0.7 percentage point lower than the same period of last year. The surveyed unemployment rate of the population with local household registration was 5% and that of the population with non-local household registration was 5.1%. Specifically, the surveyed unemployment rates of the population aged from 16 to 24 and from 25 to 59 were 15.4% and 4.2%, respectively. The urban surveyed unemployment rate in 31 major cities was 5.2%, the same as that of May. The employees of enterprises worked 47.6 hours per week on average, 0.3 hours more than in May. By the end of the second quarter, the number of rural migrant workers totaled 182.33 million.

Liu Aihua:

Ninth, resident income continued to grow and the ratio of per capita disposable income between urban and rural residents narrowed.

In the first half of this year, China's per capita disposable income of residents was 17,642 yuan, a nominal increase of 12.6% over that of last year, which was mainly due to a low base in the first half of last year. The two-year average growth rate reached 7.4%, 0.4 percentage point faster than that of the first quarter. The real growth was 12% year-on-year after deducting price factors, registering a two-year average growth of 5.2%, which was slightly slower than overall economic growth but generally growing at the same pace. In terms of permanent residence, the per capita disposable income of urban residents was 24,125 yuan, a nominal growth of 11.4% and a real growth of 10.7% year-on-year. The per capita disposable income of rural residents was 9,248 yuan, a nominal growth of 14.6% and a real growth of 14.1% year-on-year. In terms of sources of income, the income from wages and salaries, net operative income, net property income and net transfer income grew by 12.1%, 17.5%, 15%, and 9% year-on-year nominally. The per capita income of urban residents was 2.61 times that of rural residents, 0.07 less than the same period last year. The median of the nationwide per capita disposable income was 14,897 yuan, an increase of 11.6%.

In general, the national economy has sustained a steady recovery in the first half of the year, delivering a stable performance with a consolidated foundation and good momentum of growth. However, we are also aware that the global epidemic development brings many external instabilities and uncertainties, and the unbalanced recovery of the domestic economy demands more efforts to enhance the foundation for steady recovery and growth. Next, we will uphold Xi Jinping Thought on Socialism with Chinese Characteristics for a New Era as our guide, and stay committed to the general principle of pursuing progress while ensuring stability in accordance with policy decisions and plans of the Central Economic Work Conference and the Report on the Work of Government to better coordinate epidemic prevention and control with economic and social development. We will continue to deepen supply-side structural reforms and unlock the potential of domestic demand. We will step up efforts to bail out enterprises. We will accelerate reform and opening-up, and coordinate all work to ensure that the economy operates within an appropriate range. We must make solid progress in high-quality development, and redouble our efforts to fulfill the targets and tasks for economic and social development this year.

That's all for my introduction. I will now answer your questions.

Xing Huina:

Thank you, Ms. Liu. Now the floor is open to questions. Please state the name of the news outlet you work for before asking questions.

_ueditor_page_break_tag_

CCTV:

From the data just released, we note that China's average two-year growth in the first half of the year is faster than that in the first quarter. What are the factors that are driving economic growth? What's your opinion on the general performance of China's national economy in the first half of the year? Thank you.

Liu Aihua:

Thank you for your questions. The newly released data of all sectors shows that in the first half of the year, we continued to expand and consolidate the achievements in coordinating epidemic control with economic and social development, and China's economy sustained a steady recovery, delivering a stable performance with a consolidated foundation and a good momentum of growth. Its characteristics can be reflected in five aspects.

First, China's economy continued to resume growth. China's GDP expanded 12.7% year-on-year in the first half and rose 7.9% year-on-year in the second quarter, with a 1.3% increase quarter-on-quarter. Average two-year growth stood at 5.5%, 0.5 percentage point higher than that in the first quarter. Judging from the relevant indicators, the total freight volume in the first half of the year jumped 24.6% year-on-year, bringing the average growth for the past two years to 7.2%. Total electricity consumption climbed by 16.1% year-on-year, putting the average two-year growth at 7%.

Second, the economic structure was adjusted and improved. First of all, the support of industries has been enhanced. The contribution of the value added of the service sector to economic growth reached 53% in the first half of the year, 2.1 percentage points higher than that in the first quarter. The manufacturing sector cut a larger share of the GDP. The value-added of the manufacturing sector accounted for 27.9% of the GDP in the first half of the year, 1.3 percentage points higher than that in the same period last year. Besides, consumption played an increasing role in driving economic growth. In the first half of the year, the final consumption expenditure contributed 61.7% to economic growth, 42.5 percentage points higher than the contribution of the total capital formation. The consumption of upgraded consumer goods saw rapid growth. In the first half of the year, retail sales of sports and entertainment goods, communication appliances and cosmetics enterprises above designated size all registered an average two-year growth of more than 10%. Meanwhile, investment in sectors of weakness grew fast. In the first half of the year, the average two-year growth of the investment in high-tech industries and the social domain stood at 14.6% and 10.7% respectively, 10.2 percentage points and 6.3 percentage points higher than the total investment respectively. Fourth, the gap between urban and rural incomes has narrowed, with the ratio of urban and rural per capita disposable personal incomes falling to 2.61 in the first half of the year, 0.07 lower than the same period last year.

Third, innovation drivers were strengthened. First of all, new market entities registered rapid growth. The Basic Unit Database compiled by the National Bureau of Statistics at the end of June shows that the number of legal entities exceeded 30 million for the first time, up 16.6% year-on-year. Besides, new industries and new products witnessed fast growth. In the first half of the year, the value-added of hi-tech manufacturing enterprises above designated size saw an average two-year growth of 13.2%, 0.9 percentage point higher than that in the first quarter. From January to May, the total profits of hi-tech enterprises above designated size in the service sector jumped 27.4% year-on-year, with an average two-year growth of 12.5%, 4.2 percentage points higher than that of the total service enterprises above designated size. In terms of products, the output of new-energy automobiles, industrial robotics and integrated circuits sustained rapid growth year-on-year in the first half of the year. Third, new forms and models of business was growing. In the first half of the year, online retail sales of goods registered an average two-year growth of 16.5%, accounting for 23.7% of total retail sales of consumer goods. Express delivery services exceeded 50 billion items in the first half of the year, close to the level of the entirety of 2018.

Fourth, the quality and efficiency of economic performance improved in general. First of all, the ability of enterprises to make a profit was enhanced. From January to May, the total profits of industrial enterprises above designated size surged by 83.4% year-on-year, with an average two-year growth of 21.7%. The profit rate of their revenues reached 7.11%, 2.05 percentage points higher than that in the same period last year. From January to May, the total profits of enterprises above designated size in the service sector skyrocketed by 1.5 times year-on-year. Besides, the fiscal revenue continued to increase. From January to May, revenue in the general public budget grew by 24.2% year-on-year. Third, the capacity utilization rate also rose. The rate of the industrial capacity utilization stood at 78.4% in the second quarter, 4 percentage points higher than that in the same period last year, or 1.2 percentage points higher than that in the first quarter.

Fifth, the people's wellbeing continued to improve. First of all, the overall employment situation remained stable. In the first half of the year, the survey-based urban unemployment rate registered 5.2% on average, 0.6 percentage point lower than that in the same period last year, or 0.2 percentage point lower than that in the first quarter. The figure is lower than the expected target of roughly 5.5%. A total of 6.98 million new urban jobs were added, accomplishing 63.5% of the targets and tasks over the whole year. By the end of the second quarter, the number of rural migrant workers reached 180 million, basically recovering to the level of the same period in 2019. Besides, consumer prices posted a modest growth, up 0.5% year-on-year in the first half, a relatively low level of growth. Third, growth in personal income was basically in step with economic growth. In the first half of the year, per capita disposable income climbed by 12% in real terms year-on-year, with an average two-year increase of 5.2%, basically in keeping with economic growth.

Based on the five aspects mentioned above, the national economy in the first half of the year sustained a steady recovery and witnessed the consolidation of its firm growth and sound momentum. At the same time, faced with the volatile pandemic situation and many uncertainties internationally, the domestic economic recovery remains uneven and more efforts are needed to consolidate steady recovery development. In the next step, following the decisions and plans of the Central Economic Work Conference and the government work report, we will continue to deepen supply-side structural reforms, release the potential of domestic demand, help bail enterprises out, promote high-quality development, and endeavor to complete the economic and social development target and tasks throughout the year. That's all about the first question. Thank you.

_ueditor_page_break_tag_

Bloomberg:

You mentioned the income just now. My question is about the income growth. The real growth of income in the first half was 5.2% on a real average, also on a two-year average basis, which was slower than the economic growth. The Ministry of Commerce said last week in the five-year plan the retail sales will grow 5% a year through 2025. How can the economy rebalance and the dual circulations be successful, if the income and retail sales grow much slower than the overall economy? Thank you.

Liu Aihua:

Thank you for your question. Your question was mainly about income in the first half of the year. According to the statistics we just released, the nationwide per capita disposable income of residents in the first half of the year grew by 5.2%, almost the same as the average 5.3% two-year growth of GDP during the same period. Considering the impact of the pandemic, it was not easy to realize a per capita income growth of 5.2%. From the perspective of structure, there were three structural elements propelling the income growth rate to reach 5.2%.

First, with the continuous and steady recovery of the economy, the employment situation was generally stable, and growth of income from wages and salaries advanced swiftly. In the first half of the year, the income from wages and salaries grew by 12.1% year on year, with an average two-year growth of 7.2%.

Second, local governments have stepped up measures such as raising pension standards, improving basic living security for people in difficulties, and providing social relief and temporary assistance timely to meet people's living needs. Per capita net transfer income grew by 9%, with an average two-year growth of 8.6%.

Third, with the epidemic now under control, business activities gradually resumed. The statistics reflect the situation, with net business income growing by 17.5% year on year in the first half of the year and by 5.6% on a two-year average basis. The growth was attributed to the economic recovery, which propelled the increase of employment and income, policy support from local governments for ensuring people's living needs, and also endeavors from every economic entity. Based on the above-mentioned aspects, we consider these achievements remarkable as the income growth was generally in step with the economic growth.

Judging from these aspects, the internal driving force of the Chinese economy is increasing and the vitality of market entities is also growing. We hold that income growth at the next phase will also have a solid basis to provide strong support for consumption.

_ueditor_page_break_tag_

Bauhinia Magazine:

The statistics from the NBS showed that the added value of the "three new" economy, namely, new industries, new business formats, and new business models, have accounted for an increasing share of the GDP in recent years. What's your comment on the propelling effect of the "three new" economy on the overall economy? How should we promote the sustained and rapid development of the "three new" economy in the future?

Liu Aihua:

Thank you for your question. We released the statistics on the proportion of the "three new" economy against GDP last year. Here, I'll brief you first on their conditions in 2020.

Generally, against the backdrop of the great impact of the COVID-19 pandemic and the severe and complicated international situation, the new industries, new business formats, and new business models maintained rapid growth in 2020. The added value of the "three new" economy accounted for 17.08% of the country's GDP, up 0.7 percentage point year on year. The nominal growth of the "three new" economy grew by 4.5% year on year, 1.5 percentage points higher than that of the GDP growth during the same period. According to the statistics, their sustained and rapid growth and the increase of their proportion were attributed to four aspects.

First, a significant increase of scientific and technological investments. In 2020, China's R&D expenditure accounted for 2.4% of the GDP, 0.34 percentage point higher than that in 2015.

Second, the continuous expansion of scientific and technological talents. China has had the highest total number of R&D personnel in the world for the past eight consecutive years.

Third, the acceleration of scientific and technological industrialization. The integration of industrialization and informatization continues to deepen, and we have accelerated the application of research findings so that new industries keep developing rapidly. During the 13th Five-Year Plan period (2016-2020), the output of high-tech manufacturing saw an annual average growth of 10.3%, much higher than the output of industrial enterprises with annual revenue of 20 million yuan or more from their main business operations.

Fourth, the increasing support from government policies. The pandemic is a challenge but also an opportunity for the development of new industries. Our country addressed the challenge positively and turned the crisis into an opportunity by releasing a series of support measures targeting key sectors, such as accelerating the improvement of the technological innovation system with enterprises as the main body, and adopting tax reduction and exemption measures on R&D expenditure and other support policies to step up innovation and entrepreneurship. The leading role of innovation has been significantly enhanced, hence promoting the growth of new industries and new business models.

Judging from the situation in the first half of this year, the rapid growth of the "three-new" economy (new industries, new formats, and new business models) has continued. Just now I introduced to you the growth of the added value, and new products of the high-tech industry, as well as the growth of new business models. As you can see, the rapid growth of the "three-new" economy played an important role in the sustained and stable recovery of the national economy in the first half of this year. From a longer-term perspective, it also provides strong strategic support for accelerating the construction of a new development pattern. Thank you.

_ueditor_page_break_tag_

Hong Kong Economic Herald:

How should we look at the pressure of achieving peak carbon emissions and carbon neutrality targets ("dual carbon" targets) on economic operations? Some places are taking more radical measures to reduce energy consumption, such as restricting production on high-energy-consuming enterprises. Take coal power as an example, if the output limit is too large in the short term, it may cause instability in the supply of coal power, which would lead to power shortages in some regions, and also affect stable economic growth. How do you think local governments should handle the relationship between green transformation and stable growth? Thank you.

Liu Aihua:

Thank you for asking. Regarding the impact of the "dual carbon" targets on the economy in the short term, I think the current Chinese economy has shifted from a stage of rapid growth to a stage of high-quality development. Peak carbon emissions and carbon neutrality are not only our solemn commitment to the world, but also an inevitable requirement for high-quality development, and the only way to make progress in further modernization. Based on our current stage of development, we are still the largest developing country in the world and have not yet completed the process of industrialization. Given this, achieving peak carbon emissions and carbon neutrality is indeed a very heavy task with a lot of pressure.

We should realize that promoting green transformation and development may curb the short-term growth of some high-energy-consuming and high-emission industries. But at the same time, green transformation and development will also create new demands and give birth to new industries. Green industries such as energy conservation, environmental protection, and clean energy, will create new development opportunities. The green transformation and upgrading of traditional industries will also create huge market demands, so we should still seize this historical opportunity, actively respond to challenges, and promote China's economy to move steadily forward. Thank you.

_ueditor_page_break_tag_

Cover News:

I'd like to ask the spokesperson how she assesses the employment data in the first half of the year, and what the employment situation of college graduates is for this year? The data shows that the surveyed unemployment rate for those aged 16-24 reached 15.4%, an increase of nearly 2 percentage points from the end of the first quarter. How do you see this change in trend? Thank you.

Liu Aihua:

Thank you for your questions. You have just read our press release in great detail, and you have paid attention to the overall employment and structural issues. From the overall perspective of the first half of this year, the employment situation is generally stable. In the first half of the year, under the effects of a series of policies to reduce burdens, stabilize jobs, and expand employment, the surveyed national urban unemployment rate averaged 5.2% in the first half of the year – a decrease of a 0.6 percentage point from the same period last year, and a decrease of a 0.2 percentage point from the first quarter. Looking at the situations of each month, except for 5.5% in February, the other months were all below 5.5%.

The statistics of new urban job employment nationwide have already completed 63.5% of the annual target task. The surveyed unemployment rates in cities and towns in May and June were both 5%, which was a 0.7 percentage point lower than the same month of the previous year. The decline in the surveyed unemployment rate in cities and towns is mainly attributable to the continuous and stable economic recovery and employment stabilization policies. From the perspective of the unemployment rate of the main working-age population, it is even more outstanding. The unemployment rate of the main working-age population aged 25-59 fell to 4.2% in June. This was 1 percentage point lower than the same month of the previous year. From the perspective of month-to-month, it has also continued to fall.

Of course, while seeing the stability of the total amount, we must also see that there are prominent structural problems regarding employment. As you mentioned just now, with the arrival of the graduation season in June, more and more college graduates are entering the labor market for jobs, which will significantly increase the employment pressure and lead to a significant rise in youth unemployment rate. In June, the surveyed unemployment rate among urban youths aged 16-24 was 15.4%, an increase of 1.6 percentage points over the previous month, which is the same as the same month of the previous year.

Looking forward to the next stage, on the one hand, we should see that we are in a situation of epidemic prevention and control normalization, the economy is continuing to recover steadily, and the labor market is continuously picking up. Therefore, from what we currently have learned, this year's graduates have greater determination and anticipation of being employed than last year, and their job search activity has been significantly higher. But on the other hand, it is true that the number of college graduates this year has reached 9.09 million, a record high, so the employment pressure is indeed relatively high. Therefore, in the next stage, we give top priority to employment and continue to implement the policy of reducing burdens, stabilizing jobs, and expanding employment, as well strengthening employment aids to key groups, optimizing employment services, expanding employment capacity, and consolidating employment stability. Thank you.

_ueditor_page_break_tag_

CNR:

Having noted the sustained recovery of fixed-asset investment in the first half of 2021, what do you think of investment's role in stimulating economic growth? The two-year average investment growth rate still shows significant disparities compared with pre-epidemic levels. What measures should be taken to expand effective investment in the next phase? Thank you.

Liu Aihua:

Thank you for your question. You focused on the estimation of China's investment and its trends in the next phase. In terms of monthly changes, the country's investment has seen a sustained and stable recovery in the first half of this year. The two-year average growth of fixed-asset investment in the first six months was 4.4%, up 1.5 percentage points from the first quarter, which was an acceleration. Investment has played a key role in further optimizing the supply structure regarding three aspects. First, the investment in high-tech industries grew rapidly. In the first half of 2021, the two-year average growth of investment in high-tech industries rose 14.6%, up 4.7 percentage points from the first quarter, among which the growth of investment in high-tech manufacturing and service industries sped up. Second, the investment in social sectors grew rapidly, with an average two-year growth of 10.7%, 1.1 percentage points faster than that of the first quarter, among which the investment in the health sector and social work went up by more than 20%. Third, the growth of private investment also accelerated. In the first half of the year, the two-year average growth of private investment grew by 3.8%, up 2.1 percentage points from the first quarter. Investment in high-tech industries has strong kinetic energy, while the investment in the social sectors shores up weaknesses, and the private investment reflects the market vitality. With the acceleration of all of these areas, effective investment has shown to play a key role in further optimizing the supply structure.

As for the next phase, the advantages supporting continued investment recovery are increasing. First, market vitality has gradually increased. According to the profits of industrial enterprises and service enterprises above the designated size from January to May, the performance of enterprises has improved, which will enhance their confidence and ability in investment. Second, financial support is relatively strong. In the first half of the year, the funds in place for fixed-asset investment rose by 16.8% year-on-year, and the growth rate exceeded that of the investments. Third, policies to stabilize investment continue to show positive effect. A batch of major projects set out in the 14th Five-year Plan is being deployed and advanced. As we know, in June, more than 10,000 large-scale projects worth 50 million yuan ($7.74 million) and above were newly included, an increase of 11.6% from the previous month. Fourth, in the long run, new industrialization, IT application, urbanization, and agricultural modernization all offer enormous opportunities for investment. There is huge potential for investment in promoting the renovation of urban infrastructure, implementing the rural vitalization strategy, optimizing and stabilizing the industry chains and supply chains, and accelerating the transformation and upgrading of traditional industries. Therefore, we believe that investment in the next phase will continue to maintain sustained recovery on the whole. Thank you.

_ueditor_page_break_tag_

CNBC:

My question is about the impact of data in the second half of 2021, such as whether exports will continue to grow. We saw growth in the automobile consumption, which is somewhat different from June's data for the industry. What are the main factors behind this discrepancy? Thank you.

Liu Aihua:

Thank you. Let me clarify the two questions. The first is about the estimation of the growth of foreign trade. The second is about the development of the automobile industry. First of all, with regard to foreign trade outlook, relevant departments announced the data for the first half of this year a few days ago. The figures showed that China's foreign trade in the first half registered rapid growth, which is a result of many factors, including the sustainable economic recovery both at home and abroad and a relatively low base last year. The country's foreign trade rose 27.1% year on year in the first six months, an increase of 22.8% from the same period in 2019 and a two-year average growth rate of over 10%. Foreign trade in the first half of this year performed well. As for the second half, we need to pay attention to two aspects: on the one hand, we will face a certain impact on the foreign trade environment resulting from the complex situation of the global COVID-19 pandemic, the relatively high pressure of rising prices in bulk commodities, as well as the unstable external environment and many uncertain factors. On the other hand, there are more favorable conditions for foreign trade. At present, global demand is recovering, and the domestic demand is rebounding. Meanwhile, Chinese enterprises' ability to adjust to external changes has increased over the years, showing strong resilience in development. Taking these factors into full consideration, China's foreign trade is expected to maintain rapid growth for the entire year.

Second, regarding your question about the automobile industry, data in the first six months showed that, despite having fallen in the last two months, the added value of the automobile industry in the first half of 2021 increased by 21.8% year-on-year, and the two-year average growth rate increased by 8.6%. Both are faster than the growth rate of China's value-added industrial output. However, the growth of the automobile industry is also facing certain constraints spanning from chip shortages to policy adjustments, which might bring about short-term constrains such as long supply cycles and rising costs. Nevertheless, for now, there is still a gap in car ownership per thousand people between China and developed countries, which shows the automobile industry still has plenty of room to grow. In the short run, driven by the signals of rising demand and prices, the production of integrated circuits will gradually step up in spite of the complicated external environment and the time-consuming recovery of the global production capacity. Generally speaking, we assume that the automobile industry will maintain relatively fast growth in the long run. Thank you.

_ueditor_page_break_tag_

Yicai:

Since the beginning of 2021, prices of bulk commodities have been increasing, which has had an impact on the middle-and-down stream of the industrial chain and caused small and medium-sized enterprises (SMEs) to come under pressure in regards to earning profits. What are your views on price trend of bulk commodities and how should SMEs respond to this? In addition, prices of pork are continuously declining and have become the main drag for CPI. Do you believe that the pork prices have bottomed out? How do you view inflation throughout the year? Thank you.

Liu Aihua:

Thank you for your questions. You talked about at least two issues: one is about price trends among bulk commodities, and the other is related to the CPI trend.

In regard to price trend of bulk commodities: in the first six months, China's producer price index (PPI) growth averaged 5.1% year-on-year, 3 percentage points higher than that in the first quarter, according to current data. The accelerated PPI growth in the second quarter was mainly affected by the following factors: first, the economy is continuing recovering, while demand is expanding; second, it was influenced by the spike in prices of bulk commodities on the international market. This June, the global energy price index rose 92.6% year-on-year, and the non-energy price index climbed by 43.2%, with both being high; third, it was impacted by a low base over the same period last year. Affected by the pandemic, from February 2020, the PPI saw consecutive falls throughout the second quarter of last year, and the figure decreased by over 3% year-on-year for each month of the quarter. Therefore, the year-on-year growth of the PPI obviously rose in the second quarter of this year, bringing mounting cost pressures to middle-and-down stream enterprises and micro, small, and medium enterprises (MSMEs). Judging from the general situation, China boasts a strong industrial productive capacity and a sufficient supplying power in industrial products, although there remains some upward pressure caused by the surging prices of bulk commodities on the international market. Meanwhile, initial effects have been appearing as some departments recently implemented policies on safeguarding supply and stabilizing prices for bulk commodities. In June, the PPI rose 8.8% year-on-year, 0.2 percentage point slower than that was recorded in May. Therefore, the impacts of PPI growth can be generally controlled.

Your second question relates to CPI trends and the prediction of pork prices. The CPI went up moderately by 0.5% year-on-year in the first half of the year, dropping 3.3 percentage points compared to the same period in 2020, and maintained its relatively low level over the past few years. In June, the consumer prices went up by 1.1% year-on-year, 0.2 percentage point slower than in May. Declining food prices may be the main reason for the drop in CPI growth rate. Food prices decreased 0.2% year-on-year in the first half of the year, while the figure in the same period of the last year was an increase of 16.2%. Declining food prices pushed down consumer inflation in the first half of the year by 0.04 percentage point and became a main influencing factor in price fluctuations. Pork prices, as you mentioned, have been continuously decreasing for nine consecutive months, with an average drop of 19.3% in the first half of the year, pushing down consumer inflation by 0.45 percentage point. We could say that the consumer prices rose mildly in the first half of the year, with the food prices, pork prices in particular, being the main reason for the slower CPI growth.

Non-food prices, meanwhile, rose 0.7% in the first half of the year, demonstrating a similar scale with the same period of last year, pushing up the CPI by 0.57 percentage point. Energy price surges were most prominent among non-food prices, with gasoline and diesel prices rising 8.5% and 9.2% respectively in the first half of the year, which jointly push up the CPI by 0.24 percentage point. Mild CPI growth in the first half of this year resulted from the declining food prices as well as a stable growth in non-food prices.

Regarding the three categories affecting CPI in the following phases: first, food prices. China reaped a bumper summer harvest in 2021 as we noted in yesterday's announcement, and grain prices are expected to be stable this year. Pork prices are expected to remain stable as hog production continues to recover and the country's purchase and storage policies provide support. Generally speaking, food prices will face mild upward pressure under the background of a bumper summer harvest and stable pork prices.

Second, the prices of industrial consumer goods. Price hikes in bulk commodities on the international market can drive a price increase in some industrial consumer goods. However, in the long run, the market supply of industrial consumer goods will remain generally sufficient, and the prices will not generate a large-scale increase as China boasts a strong supply and industrial production capacity as well as a complete industrial system .

Third, service prices. Service prices in the first half of this year were continuously affected by the sporadic resurgence of COVID-19 cases and rose 0.3% year-on-year, remaining at a low point in recent years. In the next stage, service prices will resurge to a certain extent as the nation's pandemic prevention and control situation continues to improve; the consumption demands in catering, accommodation, and tourism gradually recover; and the market gains more confidence as well as residents' income growth rates accelerate. But in general, service prices are expected to generate a small-scale increase considering the impact of regular epidemic prevention and control.

Taking into consideration development trends in the above three categories, the prediction that prices will register a moderate rise this year is based on necessary basis and conditions, so is meeting the consumer inflation target of around 3% for the year. Thank you!

Xing Huina:

Due to the time limit, we will take the final two questions.

_ueditor_page_break_tag_

21st Century Business Herald:

China's central bank recently announced cutting the reserve requirement ratio (RRR), which is interpreted as a move to ease policies in advance so as to address the significant downward pressure that the economy will be faced with in the second half of the year. What's your comment on this? At a symposium attended by experts and entrepreneurs held a couple of days ago, Premier Li Keqiang said that we should step up cross-cyclical regulation and address some particular cyclical risks. How to make the cross-cyclical regulation work? What are the cyclical risks currently facing the Chinese economy? Thank you.

Liu Aihua:

Thank you for your question. I think your question is actually focusing on two aspects. One is about the economic outlook in the second half of this year, and the other is about the trajectory of macroeconomic policies.

Let me begin with the first question. Regarding the economic outlook, we can see from the data that the economy continued to recover steadily in the first half of this year, and the supply-demand cycle was unimpeded. The economic fundamentals have laid a good foundation for the economic performance in the second half of this year. In terms of the factors affecting the economic trajectory in the second half, the factors supporting the further recovery and improvement of the economy, in general, are gradually accumulating and increasing. First, the internal driving force for economic growth is becoming more powerful. In the first half of this year, the contribution of domestic demand to economic growth reached 80.9%, up 4.9 percentage points from the first quarter. Market sales also witnessed a steady recovery. The average growth of the total retail sales of consumer goods in the first half-year over the past two years has been 4.4%, 0.2 percentage points higher than that of the first quarter. Investment has also been recovering steadily, with investment in fixed assets seeing a two-year average growth of 4.4% in the first half-year, up 1.5 percentage points from the first quarter. It shows that domestic demand is increasingly important in promoting economic growth. Second, growing confidence among market entities has been seen. In June, the Manufacturing Purchasing Managers' Index (PMI) was 50.9%, staying above the threshold for 16 months in a row. The non-manufacturing PMI and the composite PMI output index were both considerably above the threshold, indicating greater confidence among market entities in economic growth and growth dynamics. Third, the global economy has continued on its recovery trajectory, laying a foundation for the growth of external demand. The global composite PMI for June was 56.6%, which was among the best registered over the past 15 years. Global merchandise trade volume is expected to increase by 8% in 2021, according to the World Trade Organization's most recent forecast. An 8% projection shows that global trade recovery is getting faster, which ensures that external demand will maintain rapid growth.

While the economic fundamentals, as well as supply and demand, have maintained a stable performance with good momentum for growth, macroeconomic policies have continued to provide support for the real economy and more policies have gradually been adopted to support individually-owned businesses as well as small and micro businesses. These are conducive to alleviating difficulties and solving the problems enterprises are faced with and will also inject new momentum to the market. Looking ahead to the second half of the year, many external destabilizing factors and uncertainties remain. Domestically, we have to face the reality of unbalanced economic growth, caused in part by the rising prices of the raw materials that you mentioned, which have put pressure on small and micro businesses, especially those in the middle and lower reaches, in terms of their production and operation. However, considering the general fundamentals, supply-demand cycle, market confidence, and the increasingly strong domestic demand, China's economy is expected to maintain a sustained and stable recovery in the second half of the year.

Regarding future macroeconomic policies, as I said just now, this year's overall economy will deliver a stable performance with a consolidated foundation and a good momentum for growth. On the one hand, we should be aware that the overall trend is positive. On the other hand, we should also understand that the current environment at home and abroad is complicated and that the rise in bulk commodity prices in particular, is putting great pressure on enterprises in terms of costs. Given the prominent operational problems, we should act in accordance with the decisions and deployments of the CPC Central Committee and the State Council, and focus on the present while keeping an eye on the future, ensuring cross-cyclical regulation and properly address possible cyclical risks. With a focus on fostering and boosting market entities, we need to press ahead with reforms to streamline administration, delegate power, improve regulation, and upgrade services to improve the business environment and provide more development opportunities for micro, small, and medium-sized enterprises, and lay a solid foundation for steady and sound economic growth. Thank you.

_ueditor_page_break_tag_

Ta Kung Pao and Wen Wei Po:

The data shows that the value added to enterprises funded by foreign investors or investors from Hong Kong, Macao, and Taiwan increased by 17% year on year from January to June. What is your comment on this figure? Thank you.

Liu Aihua:

Thank you for your question. You've checked the data very carefully. As you said, the value added to enterprises funded by foreign investors or investors from Hong Kong, Macao, and Taiwan increased by 17% year on year. Such a growth rate is higher than that of the industrial enterprises above the designated size. In the first half of this year, the total value added to the industrial enterprises above the designated size grew by 15.9% year on year. The 17% growth rate indicates that the investment from foreign investors and those from Hong Kong, Macao, and Taiwan have shown flexibility in responding to the economic fallout of the pandemic and adapting to the market changes. Moreover, our policies have been providing more support to enterprises and the real economy. In general, the increase of enterprises and industries invested in by foreign investors and those from Hong Kong, Macao, and Taiwan also confirms the recovery of our overall economy and indicates that the business performance of market entities is also improving. Thank you.

Xing Huina:

Thank you, Ms. Liu. Today's press conference is hereby concluded. Thank you to all of our friends from the media. Goodbye.

Translated and edited by Wang Yiming, Wang Qian, Cui Can, Yuan Fang, Duan Yaying, Chen Xia, Mi Xingang, Wang Wei, Zhang Rui, Wang Zhiyong, Zheng Chengqiong, Li Huiru, Zhang Tingting, Huang Shan, Gong Yingchun, Liu Qiang, Jay Birbeck, and Tom Arnstein and Geoffrey Murray. In case of any discrepancy between the English and Chinese texts, the Chinese version is deemed to prevail.

2ab1e45c-1324-40a7-8a8b-2aa0b9d4b420.jpg)